From the print edition | Finance and economics

www.economist.com

JEFF POWERS was raised as “a good Catholic boy”. So when he sold his wall-fastener business in 2012 for $225m, he wanted to give back. And, like many philanthropists, he started close to home. He donated to the hospital where his son had spent months recovering from a car accident. He helped pay for a swimming pool at his children’s school. Today he supports all sorts of causes, from scholarships in Florida to soup kitchens in New York.

The way Mr Powers finances these projects would strike old-school charitable types as odd. Traditionally, a budding philanthropist would either give directly to a charity or set up a foundation. But Mr Powers uses a donor-advised fund (DAF), a type of account held by a non-profit entity, in this case Bank of America Charitable Gift Fund, an arm of the bank. DAFs are taking root in Britain and Canada, but they are primarily an American phenomenon.

DAFs are way-stations for donor dollars. Mr Powers deposits some money into his DAF and, while he ponders where it should go, Bank of America invests it for him. At some point he will suggest a beneficiary and, as long as it is a charity as defined by the Internal Revenue Service (IRS), the bank makes the grant on his behalf. Mr Powers is delighted with his DAF, praising the convenience and tax advantages.

Nothing suggests Mr Powers is other than one of the many people who use DAFs for nobly philanthropic reasons. Yet not everybody is happy with these funds. A huge surge in their popularity, sparked by the entrance of financial firms to the market, is upending the philanthropic world. Sceptics say it is not clear whether DAFs actually increase the amount of money that reaches the needy, and that the tax breaks associated with them mainly benefit the rich. Moreover, opacity leaves DAFs open to abuse. One long-held concern is that they are used to sidestep rules requiring foundations to make annual donations to charities. Analysis by The Economist shows this is indeed happening.

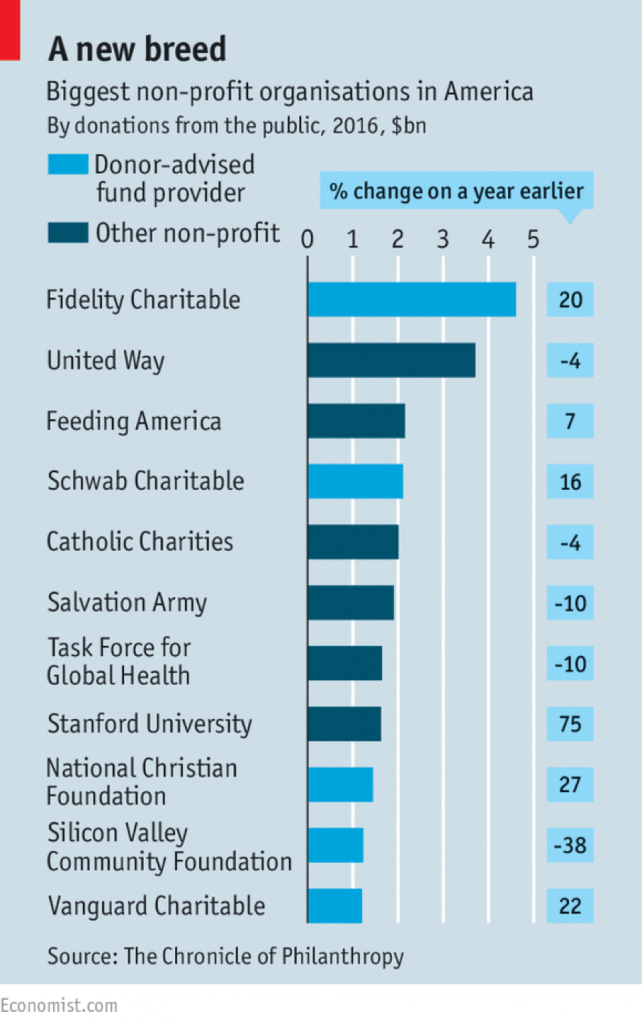

Their explosive growth is recent, but DAFs date from the 1930s. They were first used by community foundations to encourage local philanthropy as well as by single-issue non-profits, such as museums. But it wasn’t until 1969, when new reporting rules took some of the shine off foundations, that DAFs flourished. In 1991, approved by the IRS, Fidelity Charitable, a non-profit linked to the mutual-fund group, was set up to offer DAFs to clients, becoming the first commercial provider.

By 2000 many other financial firms were peddling such funds, including Schwab and Vanguard, both now DAF giants. The industry has since ballooned: from about 180,000 American DAFs in 2010 to over 270,000 in 2015, easily outnumbering foundations. The assets held in DAFs doubled in value in that time, to roughly $80bn.

Many providers have seen a further surge in donations of late, sparked in part by fears that the Trump administration may reduce philanthropic tax breaks. Between November 2016 and January 2017, Schwab saw a 68% increase in inflows compared with the same period in the previous year. Others also report a big uptick.

Even if more money is flowing into DAFs, it will not necessarily reach the needy as soon as it comes out. The Economist crunched the latest 12 months-worth of available data on the donations made by the three biggest DAF providers—the year ending June 2016 for Vanguard and the year ending June 2015 for Fidelity and Schwab (Vanguard and Schwab exclude donations under $5,000 from the data). Many payments went to worthy causes such as Médecins Sans Frontières and the Red Cross. But it is notable that the biggest recipient of DAFs’ gifts is none other than Fidelity. The third-biggest is the American Endowment Foundation, another DAF supplier. The providers say this is an innocuous rejigging of personal finances. But it supports the claim that DAFs don’t always get dollars to charities that need them.

DAFs are particularly popular among certain religions, though experts are unsure why. The Mormon church is the second-biggest recipient of DAF dollars. The American Jewish World Service and the Jewish Communal Fund rank highly, too. Fidelity allows donations only in multiples of $5 and $18, the latter being a lucky number in Judaism.

Tax breaks are an important reason why philanthropists of all stripes like DAFs. In American law donations to charities, including DAF-providers, enjoy bigger breaks than those to foundations, because the gift is seen as being put to good use immediately. Moreover, as with giving direct to charity, the tax benefits can be booked in the year of the donation, even though the ultimate beneficiary may not yet have been chosen. In a survey by Fidelity in 2015, 90% of donors named this as the main reason for starting a DAF.

Another advantage is that commercial suppliers of DAFs accept not only cash but—unlike most non-profits—illiquid gifts, such as art or land. Once a provider receives the asset, it will try to sell it and credit the proceeds to the donor’s DAF. Non-publicly traded company shares, which have risen in value, are another common gift: the tax deduction is taken at the current market value—a benefit not afforded gifts to foundations. In 2013 around 28% of donations to DAFs were non-cash.

Moreover, whereas tax laws require foundations to give out at least 5% of their assets each year, DAFs face no such condition. So donors have more time to weigh their options. DAFs are easy to use, too. Internet-banking-style platforms allow grants to be made with just a few mouse-clicks. Set-up costs are a fraction of those of foundations, without the need to hire lawyers or fill in reams of paperwork.

Fans of DAFs argue that this convenience spurs philanthropy. According to Fidelity, two-thirds of its donors say the vehicle helps them give more; other commercial suppliers cite similar figures. This does not show up in the national statistics, however. Ray Madoff, a tax expert at Boston College, points out that the share of money going to charities in America has not budged in the past decade, at roughly 2% of disposable net income (though of course, since DAFs still account for less than a tenth of total giving, many other factors could play a role in this).

The only publicly available numbers are aggregates from DAF providers. These suggest that each year around 20% of assets held by them go to good causes. This is much higher than the rate of roughly 7% seen at foundations. But this comparison is misleading. For one thing, foundations, unlike most DAFs, are set up in perpetuity and thus tend to ration their grants. For another, DAF payouts are highly uneven: in a given year around one-fifth of providers fail to make a single grant, and, as noted, some outgoings are to other DAFs. Furthermore, payout rates—the proportion of total assets leaving DAFs—are falling. Fidelity’s annual payout rate dropped from 21% to 16% between 2008 and 2014, the latest year of available data. Those of Schwab and Vanguard fell from 18% to around 11%.Weighing up the pros and cons is made harder by a scarcity of data. Numbers for individual accounts are not published—so it is impossible to know whether, for instance, thousands of donors, having collected their tax benefits, are sitting on their assets rather than distributing them.

Detractors argue that warped incentives curb giving. Providers profit from having more assets under their management and invested in their own funds. They therefore stand to gain from dissuading donors—who have already claimed their tax deductions—from making payments out of their DAF. And, because the money sitting in a DAF grows from the investment income, donors are further deterred from passing it on quickly to a good cause. (To their credit, however, the bigger DAF suppliers do have policies in place to distribute at least some of the money in dormant accounts. If an account at Fidelity has been idle for three years, it will give the holder a nudge. If the inactivity continues, Fidelity starts to make small grants on his behalf.)

Another concern is that some funds are used not to give but to game: for instance, to sidestep the 5%-minimum rule on foundation payouts. Donors can shift money from their foundation to a DAF as a way of meeting this threshold without actually giving anything to charity. The Economist examined grants from a random sample of about 4,000 foundations. Some 40 of them routed cash to the biggest DAF providers, amounting to about 1% of the value of all their contributions. This may seem like a negligible sum, but 11 of the 40 gave over 90% of the money they paid out to DAF suppliers. This is not illegal, but it does appear to flout the spirit of the tax code.

The IRS has grown wise to some of the problems. A decade ago it was including DAFs on its “dirty dozen” list of the most worrying tax scams. Another concern was self-dealing: in one case in 2006, a California-based DAF provider had boasted in its earlier marketing materials that setting up an account could “benefit the donor or the donor’s family” and that the donor’s children could be paid or granted fellowships direct from a DAF. That same year, DAFs were first defined in the tax code. Certain ruses, such as using them to buy tickets to charitable events or grant oneself low-cost loans, were later prohibited.

Although such shenanigans are harder to pull off, there are still opportunities, mainly at smaller DAF-providers, says Roger Colinvaux of Columbus School of Law. A keen fraudster could set up a small non-profit, staff it himself, channel money into a DAF, claim the tax breaks, redirect the money back to the non-profit and draw a fat, tax-advantaged salary.

Charity begins at home

Another worry is the use of DAFs to circumvent the “public-support test”. This rule stipulates that a charity typically must receive the lion’s share of its revenue from the general public. Others are classified as foundations. A creative donor could donate to a charity through numerous DAFs, giving the false impression of widespread public support. Last year, the IRS announced an investigation into this.

But the agency is stretched for resources, and experts say it struggles to keep on top of trickery. Another worry is the use of DAFs to convert illiquid assets, such as property or hard-to-price securities, into charitable dollars. Some fear the valuation system is open to abuse. Donors, who are keen to get the best price and maximise tax deductions, typically hire a third party to do the valuation. Monitoring this process is time-consuming and costly, and thus rarely carried out. A study by the Treasury Inspector General for Tax Administration, an American watchdog, looked at a sample of non-cash gifts to charities in 2010. It found that around 60% of returns did not meet reporting requirements and none of these had been examined by the IRS.

Moreover, DAFs are frequently used to funnel money to political campaigns and lobby groups, rather than what most people would consider good causes. Donors to such groups can also exploit the funds’ murky nature to hide their identity. One study by Robert Brulle of Drexel University, in Philadelphia, tracked contributions to the anti-climate-change lobby in America. He found that in 2009 and 2010 about a quarter of its backing which could be traced came via the Donors Trust, a Virginia-based DAF supplier. There is no way of telling where this money originated.

Fans of DAFs argue that such cases are exceptions, and that most of their money goes to uncontroversial good causes. Many give generously and sincerely. But concerns will linger that DAFs allow the rich to reap financial benefits from financing pet causes they might well have backed anyway—and that more advantages accrue to donors than to the causes they are supposed to be helping. At present, there is scant evidence to suggest they fuel an overall rise in giving. Many philanthropists sing DAFs’ praises. But that does not prove their worth to society as a whole.